35,000+ smart investors are already getting financial news, market signals, and macro shifts in the economy that could impact their money next with our FREE weekly newsletter. Get ahead of what the crowd finds out too late. Click Here to Subscribe for FREE.

Most Canadians think they understand their bank accounts. Statements arrive, balances look familiar, and nothing seems off at first. The problem is not the obvious charges. It is the quiet ones who blend into routine. Small fees repeat monthly, annual charges renew automatically, and penalties appear without warning. By the time most people notice, the money is already gone. Here are 16 Bank Fees Canadians Didn’t Notice Until It Was Too Late.

Monthly Account Maintenance Fees

16 Bank Fees Canadians Didn’t Notice Until It Was Too Late

- Monthly Account Maintenance Fees

- Out-of-Network ATM Withdrawal Fees

- Excess Transaction Fees

- Interac E-Transfer Fees

- Overdraft Protection Fees

- Non-Sufficient Funds Fees

- Credit Card Annual Fees

- Foreign Transaction Fees

- Paper Statement Fees

- In-Branch Service Fees

- Account Closing Fees

- Dormant Account Fees

- Balance Inquiry Fees

- Cheque Processing Fees

- Early Investment Withdrawal Fees

- Currency Conversion Markups

- 22 Groceries to Grab Now—Before another Price Shock Hits Canada

Monthly account maintenance fees often appear small and harmless at first glance. Many chequing accounts waive them only if balances stay high. A single low balance month can trigger repeated charges. Banks rarely send alerts before applying the fee. Over a year, these charges quietly add up. Students and seniors often lose discounts after status changes. Some accounts charge different rates by province. Customers notice only when statements look wrong. Switching accounts later feels inconvenient. The fee keeps running meanwhile. This is one of the most common costs Canadians overlook until long after the damage is done for many people.

Out-of-Network ATM Withdrawal Fees

Using the wrong ATM can cost more than expected. Canadian banks charge their own withdrawal fee first. The ATM owner then adds another charge. These fees stack instantly. Tourists and small-town residents get hit most often. Many machines do not clearly show total costs upfront. Receipts come later, when the damage is done. Frequent cash users feel this pain monthly. Over time, these withdrawals become expensive habits. People rarely track them individually. They feel minor in isolation. Combined, they quietly eat into budgets. Canadians often realize the total only after reviewing yearly statements with frustration and surprise.

Excess Transaction Fees

Many chequing accounts limit monthly transactions. Going over that number triggers per-use charges. Debit purchases, bill payments, and transfers all count. People rarely track their totals. Automatic payments make it worse. The fee often appears days later. Some banks charge higher rates for in-branch activity. Digital banking does not always protect users. Busy months add extra costs without warning. Families feel this during holidays. New parents notice it quickly. These fees seem random at first. They are not. They are predictable costs that quietly grow until customers finally connect the dots too late.

Interac E-Transfer Fees

E-transfers feel free because they are digital. Many accounts still charge per transfer. Some banks allow only limited free sends. Others charge after a monthly cap. Receiving money can also incur fees. Small transfers feel harmless. Frequent users pay repeatedly. Splitting rent, sharing meals, or selling items adds up. Statements rarely highlight these charges clearly. Canadians assume modern tools are free. That assumption costs money. Over months, fees pile up quietly. People notice only after reviewing totals. By then, habits are already formed and difficult to change without switching accounts entirely.

Overdraft Protection Fees

Overdraft protection sounds helpful and safe. It is not free. Banks charge a fee each time it is used. Interest starts immediately. Some charge monthly access fees, too. Small overdrafts trigger full charges. A coffee purchase can cost much more later. Many Canadians forget they enabled this service. Others assume it works like a buffer. It does not. Repeated use becomes expensive quickly. Statements rarely clearly explain the total cost. People notice only after the balances struggle to recover. Overdraft protection often costs more than declining transactions, especially for those living paycheque to paycheque.

Non-Sufficient Funds Fees

NSF fees hit hard and fast. A single missed payment can cost over forty dollars. Bills bounce without warning. Banks charge instantly. The merchant may charge separately. Multiple payments can fail in one day. That creates repeated fees. Many Canadians do not receive real-time alerts. Timing issues cause accidental overdrafts. Rent days are risky. Pay delays make things worse. These fees punish short-term cash gaps. People notice them only after the account is already damaged. Recovering takes time. NSF fees often start chains of financial stress that feel sudden but were quietly waiting.

Credit Card Annual Fees

Annual fees feel distant at signup. The first year is often free. Renewal happens automatically later. Charges appear quietly on statements. Many forget that the card even has a fee. Others assume benefits justify the cost. Usage does not always match promises. Cashback caps reduce value. Travel perks go unused. Points expire quietly. Canadians realize the mismatch too late. Canceling becomes inconvenient. Fees already posted rarely get reversed. Over the years, these costs grow unnoticed. Cards stay open out of habit. Annual fees quietly drain money from accounts without providing equal value in return.

Foreign Transaction Fees

Foreign transaction fees apply beyond travel. Online shopping triggers them too. Streaming services and apps can qualify. Banks charge a percentage per purchase. Conversion rates add another layer. Many statements hide these costs within totals. Small purchases still carry fees. Frequent international spending adds up fast. Canadians notice only when the totals feel high. Travel cards help, but not everyone uses them. People assume exchange rates explain the difference. Fees are often the real culprit. These charges repeat quietly until someone compares amounts closely. By then, months of spending have already passed unnoticed.

Paper Statement Fees

Paper statements feel old-fashioned and harmless. Many banks now charge for them. Fees appear monthly or per mailing. Customers rarely notice immediately. Automatic payments hide the charge. Seniors are affected the most. Opting out requires account changes. Some people value physical records. That preference now costs money. Banks rarely highlight this fee clearly. Over a year, the cost feels unnecessary. Canadians often discover it by accident. Switching to digital later feels obvious. Unfortunately, the money already spent cannot be returned. Paper statements quietly cost more than most people expect today.

In-Branch Service Fees

Walking into a branch can cost money. Teller transactions sometimes carry fees. Deposits, transfers, and bill payments may not be free. Banks encourage digital use quietly. Customers learn this only after charges appear. Some accounts allow limited free visits. Others charge every time. Seniors and rural residents face this often. Complex issues require in-person help. That help comes at a price. Canadians trust branches without question. Statements later tell a different story. In-branch fees feel unfair after the fact. By then, habits are already built around face-to-face service.

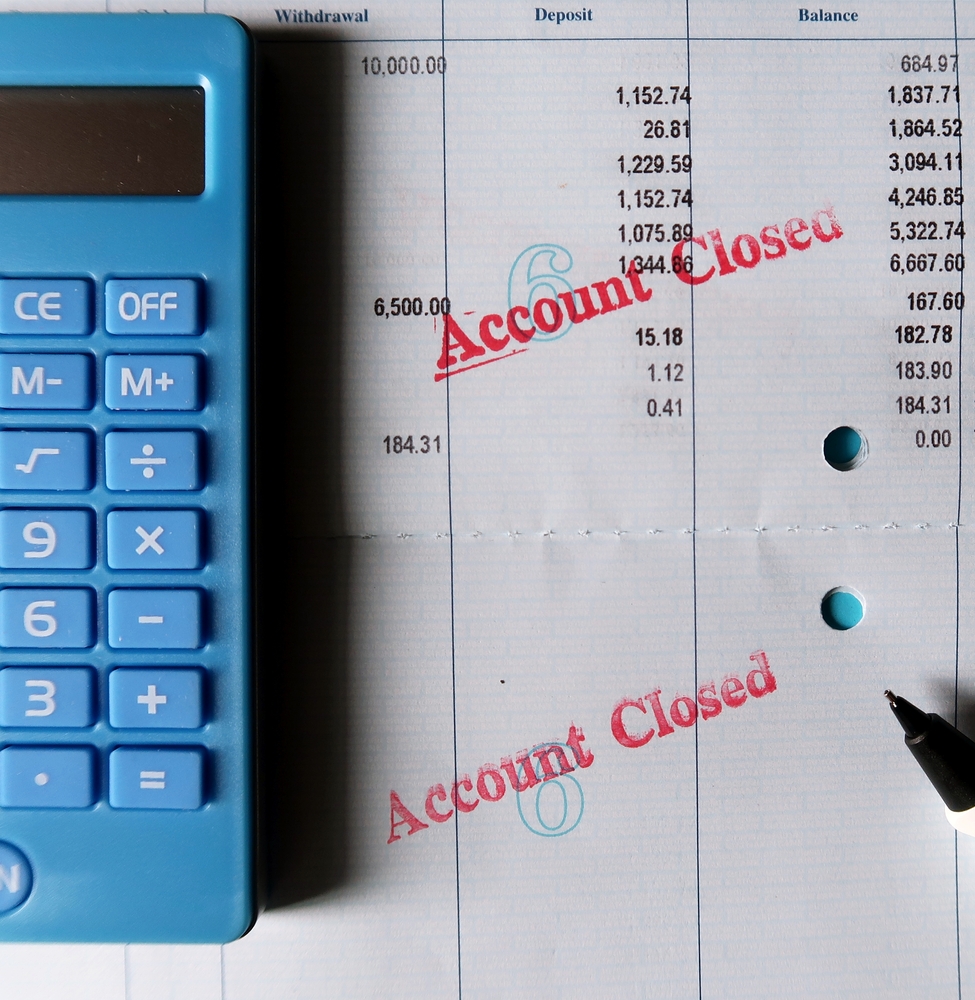

Account Closing Fees

Closing an account feels like a clean break. Some banks charge for it. Fees apply if accounts close too soon. Promotions often include hidden timelines. Moving banks triggers unexpected costs. Customers assume leaving is free. Statements prove otherwise later. Fees may apply to savings or investment accounts, too. The charge often appears after closure. That makes disputes harder. Canadians notice only when balances drop unexpectedly. Switching banks should feel simple. These fees make it stressful. Many people stay longer than planned to avoid them. Others pay without realizing the cost until it is already gone.

Dormant Account Fees

Inactive accounts do not stay free forever. Banks charge for long periods of inactivity. Small balances shrink quietly over time. Students and movers are affected most. Forgotten accounts slowly drain. Notices may arrive by mail or email. Many never see them. Fees continue regardless. Canadians rediscover accounts years later. The balance looks shockingly low. Recovery options are limited. The bank followed its policy. Dormant fees feel invisible until rediscovery. By then, most of the money is gone. These fees punish forgetfulness more than misuse, and they often catch people completely off guard.

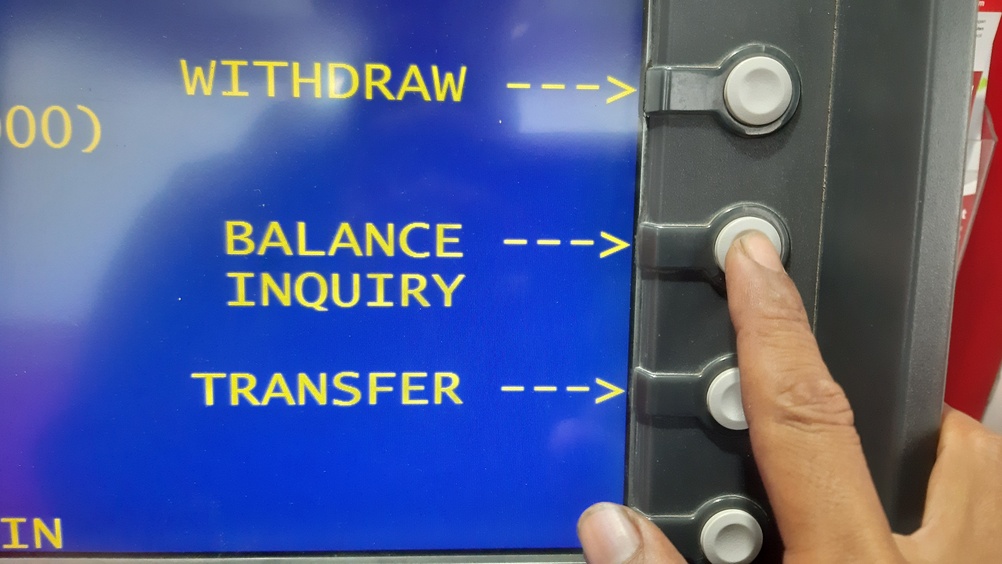

Balance Inquiry Fees

Checking a balance sounds harmless. Some ATMs charge for it. Using non-bank machines increases risk. Fees apply even without withdrawals. People assume only cash costs money. Statements reveal otherwise later. Frequent checks create repeated charges. Travelers are hit hardest. Limited access pushes people to unfamiliar machines. Banks rarely explain this clearly. Canadians notice only when statements show unexplained small fees. Each one feels insignificant. Together, they add up. Balance inquiries feel necessary. Paying for them feels unfair afterward. Many people stop checking balances only after realizing the cost was quietly growing.

Cheque Processing Fees

Cheques feel outdated but still exist. Processing them can cost money. Some banks charge per cheque written. Others charge for deposits. Business accounts face higher rates. Personal accounts are not immune. Fees appear days after processing. Canadians assume cheques are free. Older habits create hidden costs. Rent and reimbursements trigger these charges. Statements list them without explanation. People notice months later. Cheque fees feel avoidable in hindsight. Unfortunately, the money is already gone. These costs persist quietly until someone switches fully to digital payments and reviews past statements carefully.

Early Investment Withdrawal Fees

Investment accounts promise flexibility. Withdrawals often carry penalties. Timing matters more than people realize. Selling too early triggers fees. Market losses add pain. Banks disclose rules in fine print. Many Canadians skim those details. Emergencies force quick decisions. Fees apply automatically. Statements show reduced payouts later. People blame markets instead. Some charges relate to the account type. Others depend on holding periods. These fees are rarely explained clearly at withdrawal. By the time funds arrive, the cost is already deducted. Canadians learn the lesson only after money disappears unexpectedly.

Currency Conversion Markups

Currency conversion includes more than exchange rates. Banks add markups quietly. The rate shown is rarely the rate used. Cards convert automatically at purchase time. Customers see the result later. Comparing rates takes effort. Most people do not bother. Frequent travelers pay repeatedly. Online shoppers notice inconsistent totals. Statements rarely break down the markup. Canadians assume currency shifts explain differences. Markups are the real reason. Over time, these costs add up significantly. People realize only after comparing tools or switching banks. By then, years of purchases have already absorbed unnecessary fees.

22 Groceries to Grab Now—Before another Price Shock Hits Canada

Food prices in Canada have been steadily climbing, and another spike could make your grocery bill feel like a mortgage payment. According to Statistics Canada, food inflation remains about 3.7% higher than last year, with essentials like bread, dairy, and fresh produce leading the surge. Some items are expected to rise even further due to transportation costs, droughts, and import tariffs. Here are 22 groceries to grab now before another price shock hits Canada.

22 Groceries to Grab Now—Before another Price Shock Hits Canada

This Options Discord Chat is The Real Deal

While the internet is scoured with trading chat rooms, many of which even charge upwards of thousands of dollars to join, this smaller options trading discord chatroom is the real deal and actually providing valuable trade setups, education, and community without the noise and spam of the larger more expensive rooms. With a incredibly low-cost monthly fee, Options Trading Club (click here to see their reviews) requires an application to join ensuring that every member is dedicated and serious about taking their trading to the next level. If you are looking for a change in your trading strategies, then click here to apply for a membership.