35,000+ smart investors are already getting financial news, market signals, and macro shifts in the economy that could impact their money next with our FREE weekly newsletter. Get ahead of what the crowd finds out too late. Click Here to Subscribe for FREE.

Interest rates are moving again, and spring often brings a fresh wave of mortgage decisions across Canada. Some borrowers rush to lock in, fearing the next announcement. Others wait, hoping for better terms. Both reactions can cost money if they skip the fine print. A rate is more than a number on a website. It connects to penalties, flexibility, and long-term plans. Before signing anything, pause and ask sharper questions. The right ones can protect thousands of dollars over a few years. Here are 14 questions Canadians should ask before locking a rate this spring.

How long do I realistically plan to keep this mortgage?

14 Questions Canadians Should Ask Before Locking a Rate This Spring

- How long do I realistically plan to keep this mortgage?

- What are the penalties if I break this mortgage early?

- Is this rate fixed or variable, and what does that mean for my budget?

- What is the total cost over the full term?

- Are there prepayment privileges, and how flexible are they?

- Can I port this mortgage if I move?

- What happens if rates drop after I lock in?

- Is the lender federally regulated or provincially regulated?

- Are there any hidden fees or conditions?

- How will this mortgage affect my long-term financial goals?

- What is the amortization period, and can it change?

- How stable is my income right now?

- What assumptions am I making about future rates?

- Have I compared multiple lenders and brokers?

- 22 Groceries to Grab Now—Before another Price Shock Hits Canada

Five years sounds standard, but your life may not follow that script. Are you planning to move for work? Is a larger home on the horizon? If you expect changes within three years, a long-fixed term could backfire. Breaking a mortgage early often triggers steep penalties. Those costs can wipe out savings from a lower rate. On the other hand, if stability matters and you plan to stay put, a longer term may fit better. Match the mortgage term to your real timeline, not the promotional headline.

What are the penalties if I break this mortgage early?

Many Canadians focus only on the interest rate. Penalties deserve equal attention. Fixed-rate mortgages often use an interest rate differential formula. That calculation can produce a bill in the thousands. Variable rate mortgages may charge three months of interest instead. Ask your lender for a written estimate based on today’s rates. Compare scenarios before signing. If you might refinance, sell, or restructure debt, flexibility matters. A slightly higher rate with lower penalties could cost less overall if life changes quickly.

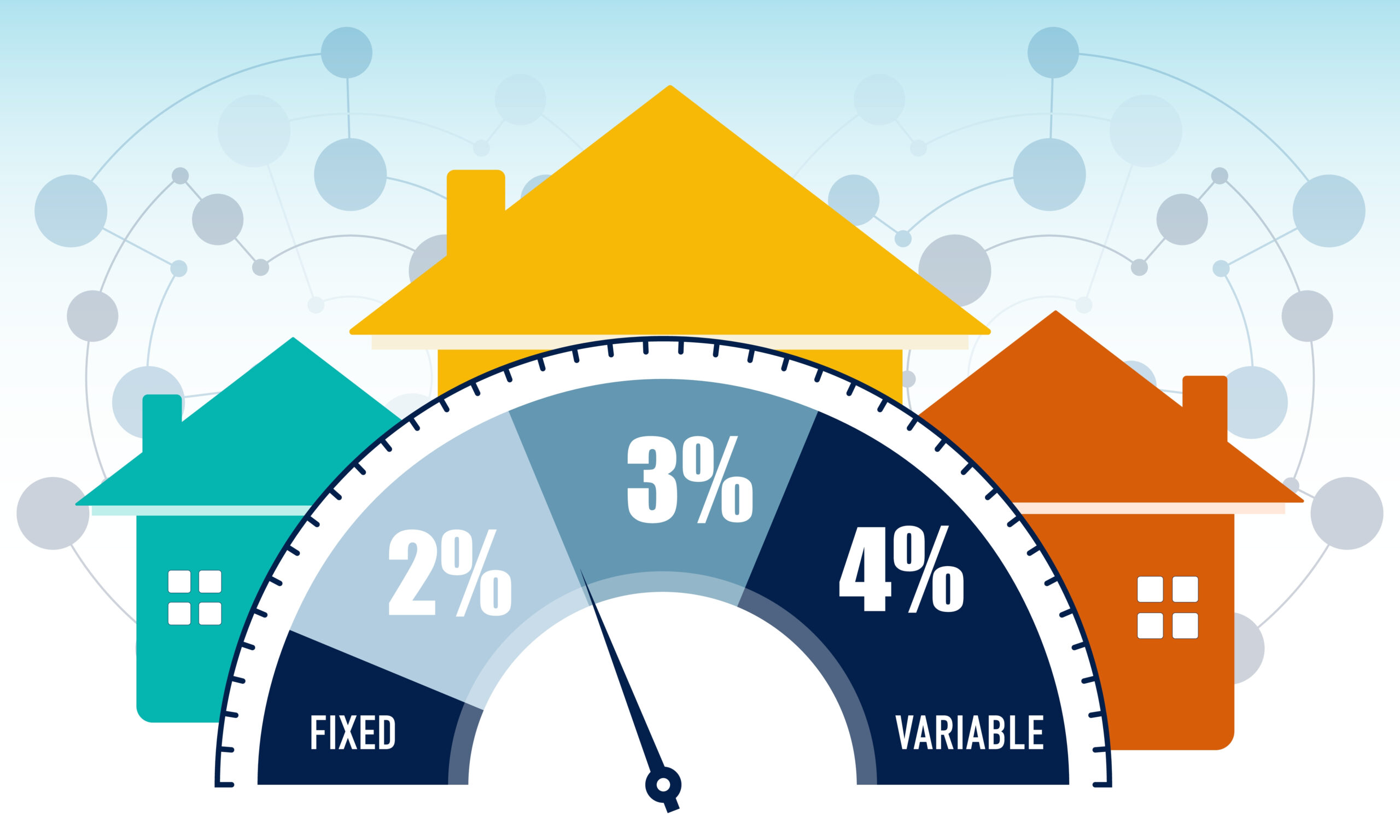

Is this rate fixed or variable, and what does that mean for my budget?

A fixed rate keeps payments predictable. A variable rate can move with the lender’s prime rate. When rates fall, variable borrowers may save. When rates rise, payments or amortization can increase. Ask how payment changes are handled. Will your monthly amount rise immediately, or will more go toward interest? Understand your comfort with risk. If a surprise payment hike would strain your budget, stability might matter more than chasing savings. Choose based on your cash flow tolerance, not headlines alone.

What is the total cost over the full term?

A lower rate does not always mean lower total cost. Ask for an amortization schedule. Review how much interest you will pay over the term. Compare two offers side by side. Include lender fees and any cash back conditions. Some promotions offer cash up front but attach higher penalties. Others may bundle insurance products. Look beyond monthly payments. The full-term cost tells a clearer story. A small rate difference can add up to thousands over five years.

Are there prepayment privileges, and how flexible are they?

Prepayment options can shorten your mortgage life. Many lenders allow annual lump sum payments. Some permit payment increases within limits. Ask about the percentage allowed each year. Check whether the unused room carries forward. If you expect bonuses or irregular income, flexibility helps. Without prepayment privileges, extra payments may trigger penalties. Over time, strategic lump sums can cut years off your amortization. That saves significant interest. Review the rules carefully before committing to a term.

Can I port this mortgage if I move?

Portability allows you to transfer your mortgage to a new property. Not all mortgages offer simple portability. Even when allowed, timelines can be strict. You may need to close both transactions within a short window. If your next home costs more, blending rates may apply. That process can be complex. Ask how porting works in writing. If you plan to upgrade within a few years, portability can prevent penalties. Without it, selling early could become expensive.

What happens if rates drop after I lock in?

Spring rate decisions can shift quickly. Once you sign, you may not benefit from later cuts. Some lenders offer a ” float down ” option before closing. That allows you to access a lower rate if it becomes available. Ask if this feature exists and how it works. Check deadlines and conditions. If there is no float down, weigh your timing carefully. Locking in too early could limit flexibility. Waiting too long could expose you to increased risk.

Is the lender federally regulated or provincially regulated?

Regulation affects how complaints and rules are handled. Federally regulated lenders follow national guidelines. Provincially regulated lenders follow provincial frameworks. Both can offer competitive products. Still, protections and complaint processes differ. Ask who oversees the lender. Research their reputation. Read recent customer reviews. Stability matters when you commit to a multi-year contract. A slightly better rate may not justify dealing with a lender that lacks transparency or strong service standards.

Ask directly about administration fees, discharge fees, and appraisal costs. Some lenders charge for transferring your mortgage elsewhere. Others require you to purchase insurance products. Review the commitment letter carefully. Look for clauses about rate holds or funding conditions. Do not rely on verbal assurances. Get every detail in writing. Small fees can add up, especially when refinancing later. Clear documentation protects you from unpleasant surprises at closing.

How will this mortgage affect my long-term financial goals?

Your mortgage should support broader plans. Consider retirement savings, education funds, and emergency reserves. A lower payment might free up cash for investing. A shorter amortization might reduce long-term interest. Ask how different payment options affect your monthly budget. Avoid stretching so far that you cannot save elsewhere. Balance matters. A mortgage is a major obligation, but it should not crowd out every other financial priority you have.

What is the amortization period, and can it change?

Amortization determines how long it will take you to repay the loan. A longer amortization lowers monthly payments. It increases total interest paid. Ask whether the amortization can be extended later. Some variable mortgages automatically extend when rates rise. That can delay repayment. Others allow you to shorten the schedule with higher payments. Understand how your balance will decline over time. Review projections. Small adjustments now can influence your financial picture for decades.

How stable is my income right now?

Spring optimism can hide income risks. Are you on contract, probation, or commission-based pay? Is your industry facing layoffs or restructuring? A fixed rate may provide stability during uncertain periods. A variable rate may require more flexibility if payments change. Consider the size of your emergency fund. If you lack a strong cushion, predictable payments may matter more. Be realistic about upcoming expenses. Mortgage stress often begins with income disruption, not rate changes. Choose a structure that fits your current financial stability.

What assumptions am I making about future rates?

No one can predict rate movements with certainty. Headlines often drive emotional decisions. Ask yourself why you prefer a fixed or variable option. Are you reacting to the fear of increases? Are you assuming cuts will happen quickly? Challenge those beliefs with facts. Review how rates have moved historically. Timing the market is difficult, even for professionals. Focus on what you can control instead. Payment comfort and flexibility usually matter more than guessing correctly about the next announcement.

Have I compared multiple lenders and brokers?

Relying on one offer can limit your options. Rates, penalties, and privileges vary widely across lenders. Mortgage brokers often access products that banks do not advertise publicly. Some lenders compete aggressively for new clients. Others prioritize existing relationships. Request written quotes from at least three sources. Compare terms carefully, not just interest rates. Ask about penalties, portability, and prepayment rules each time. Even a small rate difference can translate into thousands saved over a full mortgage term.

22 Groceries to Grab Now—Before another Price Shock Hits Canada

Food prices in Canada have been steadily climbing, and another spike could make your grocery bill feel like a mortgage payment. According to Statistics Canada, food inflation remains about 3.7% higher than last year, with essentials like bread, dairy, and fresh produce leading the surge. Some items are expected to rise even further due to transportation costs, droughts, and import tariffs. Here are 22 groceries to grab now before another price shock hits Canada.

22 Groceries to Grab Now—Before another Price Shock Hits Canada

This Options Discord Chat is The Real Deal

While the internet is scoured with trading chat rooms, many of which even charge upwards of thousands of dollars to join, this smaller options trading discord chatroom is the real deal and actually providing valuable trade setups, education, and community without the noise and spam of the larger more expensive rooms. With a incredibly low-cost monthly fee, Options Trading Club (click here to see their reviews) requires an application to join ensuring that every member is dedicated and serious about taking their trading to the next level. If you are looking for a change in your trading strategies, then click here to apply for a membership.